Taking a look at developments in Europe

On March 25, 2019, Apple announced its entrance into a new line of business: credit cards. The foray of this tech titan into the payments industry is just the latest sound bite in the ongoing disruption of the payments industry. Major banks, credit companies and financial giants have historically controlled payments, but that dominance has been challenged by technologies such as blockchain and mobile pay. [1] Regulatory changes, customer data and privacy issues, and next-generation payment methods are paving the way for a full-scale transformation of the financial services industry.

In this article, we take a look at shifts in the payment industry in Europe and how a more decentralised, technology-driven system may shift this US$100 trillion plus market1 around the world.

Changes to the traditional payment model

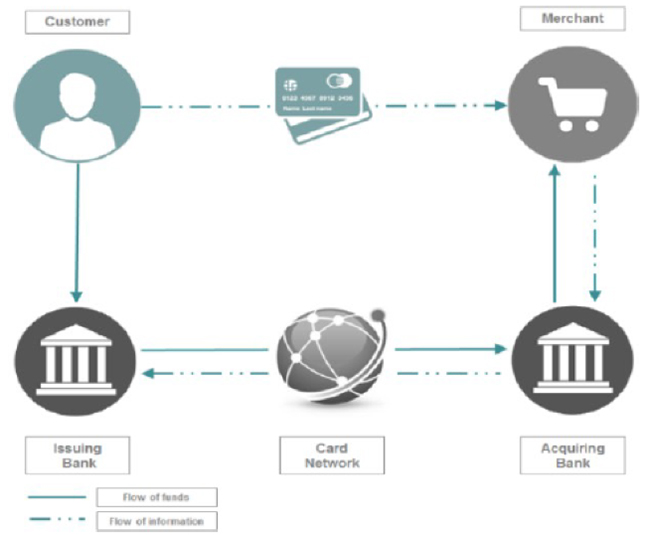

The primary revenues coming from the payment industry traditionally include:

Merchant acquiring fees. Fees charged by the bank or financial institutions that process credit or debit card payments on behalf of a merchant.

ssuer service fees. Fees paid to the issuer of the credit or debit card.

Foreign exchange fees. Fees charged on purchases that pass through a foreign bank.

Figure 1. Current Payments Model [2]

Messenger applications, payment firms and cash-less, card-less payment solutions at the point of sale are disrupting traditional payment models. Blockchain and other technologies are bypassing financial institutions altogether by enabling direct payments between parties. In Europe, the Revised Directive on Payment Services (PSD2) weakens the monopoly banks have long held on customer data and direct-to-consumer relationships.1 Now, merchants or processing companies can directly access customer account information. This not only makes payments faster and more efficient, but also gives processing companies the ability to share customer spending insights with merchants.

Unique aspects of the payments market in Europe

Europe differs from other geographies in a number of ways:

Europe is much more skewed to debit card than credit card payments.

While Visa, Mastercard and American Express dominate the market in the US and the UK, Europe has a more diverse set of payments methods, which increases complexity for payment service providers.

PSD2 is unique to Europe.

Trust, convenience and regulatory moats remain a key defence for banks’ core product offering and revenue streams, but payments and the data opportunity that comes with the implementation of PSD2 represent a potential bridgehead for fintech in retail banking. [3] In Europe, new players such as Wirecard and Ayden can offer merchants cheaper, better payment processing via efficient global platforms. Greater use of mobile wallets—with store cards that facilitate direct bank to bank payments (rather than bank-issued cards)—could erode debit and credit card usage, putting issuer fees at risk.

With the rise of online retailing and global e-commerce, merchants are increasingly seeking the ability to accept payments across multiple payment systems in Europe. This requires technological complexity, as well as investment in software and analytics to reduce fraud and to increase conversion rates. Best-in-class payment service providers will also need to provide simple integration into merchants’ back end systems, along with value-added services around data and revenue optimisation.

As banks in Europe face challenges from new, technology-driven entrants in payment services, our analysts are seeing banks pursue new strategies to protect value:

Improved merchant solutions offerings. Banks currently have a much larger share of the global offline business of merchants, and some are now adapting their offerings to provide improved online merchant solutions.

Acquisitions of and partnerships with new entrants. Banks may consider merging or partnering their payments business with a scale player.

Outsourcing arrangements. Rather than building their own technology, banks may benefit from outsourcing to or sourcing white label technology from technology-led payments companies.

Disrupting the existing system to retain control. Given the legacy nature of the payments infrastructure in many banks, this can be an expensive and long-term strategy, but could be a route to developing market leading capability.

We expect to see strong market growth in the payments industry being driven by the shift from cash to cards. In an increasingly complex payments landscape, non-bank players—which operate on more modern platforms and with fewer barriers to innovation than banks—are well-positioned to take market share, particularly for cross-border payments. Over the next few years, increased collaboration amongst banks and technology companies will reshape the customer experience, transforming the payments industry and, potentially, the broader financial services landscape.

For more on how FinTech companies are disrupting the payments industry or a copy of our report, speak to your Morgan Stanley financial adviser or representative. Plus, more Ideas from Morgan Stanley’s thought leaders.

1. Forbes. Five Reasons The Payments Business Is Ripe For Big Change, September 19, 2018.

2. Morgan Stanley Research.

3. Morgan Stanley Research.