The US may be in the middle of what could be a 20-year secular bull market for equities that began in 2011.

Morgan Stanley acknowledges a recession in the near term, believing markets are in the midst of a cyclical consolidation. However in the longer term, it is likely the US is still in the middle of what could be a 20-year secular bull market for equities that began in 2011.

Secular bull market

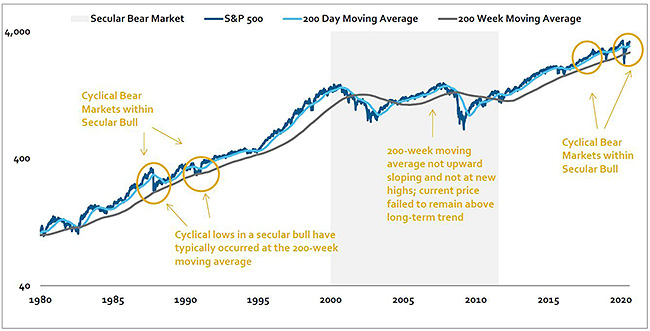

Morgan Stanley defines a secular bull market as one in which the long-term trend line is sloping upward, and the current price of the S&P 500 is above the long-term trend. In secular bull markets, stocks tend to rise more than they fall, drawdowns are relatively shallow and recoveries from pullbacks are relatively rapid.

S&P 500 price since 1980

Daily data as of 6 August 2020

Source: Bloomberg, Morgan Stanley & Co. Research

While cyclical bear markets and economic recessions can occur within secular bull markets, the magnitude or length of such pullbacks has been much less severe in secular bulls versus secular bears. As a result, Morgan Stanley does not believe the current cyclical downturn will be as prolonged as those seen in 2000 and 2007, from either a market or economic perspective, as those downturns occurred during a secular bear market.

Over the past century, US equities have progressed through five long-term, or secular, market phases. Morgan Stanley believes US equities are in the midst of a sixth phase, a secular bull market that began with the recovery from the Great Recession in 2011.

Each secular period has been characterised by a paradigm shift, which has been driven by a combination of demographic shifts, technology innovations, and significant regulatory or monetary policy regime changes.

Powering the next phase of the secular bull market

The current secular bull has had two distinct phases. Morgan Stanley believes the first phase (2010-2019) was characterised by financial repression and financial engineering driving returns.

The second phase, which is beginning now, will likely be powered by:

- Prime earning age population bouncing back – As the Millennials reach peak working age and Generation Z begins to enter the workforce, the deceleration and contraction of prime earners will likely reverse, boosting the consumer’s ability to spend.

- The strength of a demographic tailwind – Demographics can provide a powerful tailwind to markets. The previous major demographic impulse in the US was from the Baby Boom generation, which turned 35 and entered the prime earning age in 1981. The current generational impulse, the Millennials, turned 35 in 2016.

- Labour force participation picking back up – Following nearly two decades of decline in the labour force, the participation rate has stabilised in recent years and has even begun to move higher; as working age population in the US is set to grow, coupled with more favourable dynamics in the participation rate, a growing labour force could serve as a meaningful tailwind to US economic growth in the coming decade.

- Productivity turnaround – Productivity appears to be picking up, driven by the Fourth Industrial revolution. Research and development spending as a percentage of GDP is expanding as well, and now exceeds levels from the 1980s.

The bottom line: portfolio implications

Despite the potential headwinds Morgan Stanley sees for portfolios in the next 12-24 months, investors should keep in mind the context of the secular bull.

Cyclical bear markets and recessions can occur during secular bull markets, but they are less likely to be the prolonged financial and economic calamities that characterised 2001 and 2008. Prudent risk management and planning is important, but investors should be wary of overreacting to market events, especially those with long time horizons.

For more on the secular bull market, speak to your Morgan Stanley financial adviser or representative. Plus, more Ideas from Morgan Stanley's thought leaders.