Issues around migration, debt, and inflation are likely to persist after the direct virus impacts have eased.

Australia is likely to have a shallower near-term downturn and perform relatively well compared to some other advanced economies. This is due to the structure of its economy, positive case trajectory and the relatively lighter lockdown measures put in place.

There are three key issues, however, that are likely to weigh on the recovery: migration, debt and inflation.

Migration: Are we losing a key growth driver?

It’s a well-known fact that migration and population growth are key growth drivers for a country.

For much of the past decade, Australia has had a strong migration program, with net migration averaging around 250,000 each year. This has been a significant contributor to underlying demand growth.

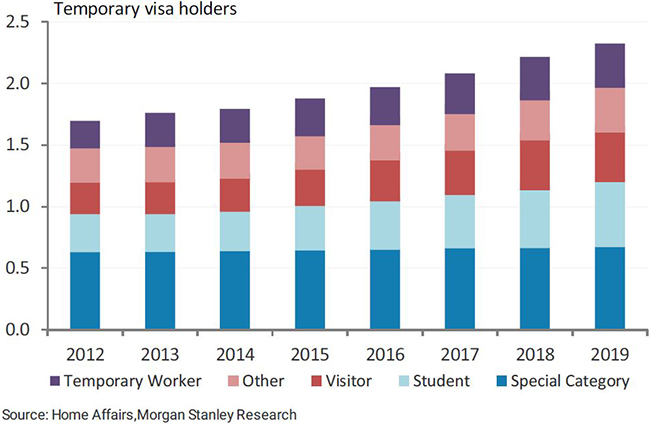

While there are specific quotas around gross permanent migration, the majority of net migration over the past decade has been driven by a significant expansion in temporary migration – in particular students and their related visas. At the end of 2019 there were around 2.3 million temporary visa holders in Australia – up significantly from the 1.7 million in 2012.

Morgan Stanley Research is sceptical that this can continue and see signs that a lower level of migration and population growth would cause a sustained, broad-based decline in several sectors, including in the housing and education market.

Exhibit 1: There are 2.3 million temporary visa holders in Australia, meaning any change will have a significant impact on net population flows

Due to restrictions on international travel, the growth in temporary visa holders will reverse in the short term, as inflows slow substantially and some existing holders decide to return to their home countries.

If we look at housing specifically, a lower population growth rate reduces the demand for housing, and due to the COVID-19 effects, this is likely to occur alongside a higher unemployment rate and higher household sizes as people move back home. We’re also likely to see a large shift in the stock of short-term accommodation to long-term rentals. All of these factors point to an excess supply of housing, particularly in the rental market, which leads vacancy rates to increase and rents to fall. This could flow through into broader house price declines, particularly when current government and bank assistance policies are removed later in the year.

Debt: Governments borrowing, households paying down

The COVID-19 crisis has sharpened the focus on debt levels and profiles of the different sectors in the economy. These are likely to have an important impact on Australia's recovery profile.

The initial focus is on the government debt profile. The Australian Government is expecting to increase its level of debt significantly, reflecting the large stimulus package of around 10% of GDP. Three factors are likely to help the sustainability of this package:

Government accounts were in good shape prior to this crisis – gross government debt was 42.7% of GDP and the budget was balanced.

The RBA is implementing yield curve control, which means it will purchase as much government debt as is needed to keep the government's borrowing costs low.

The stimulus measures are explicitly temporary – most of the measures provided last only six months.

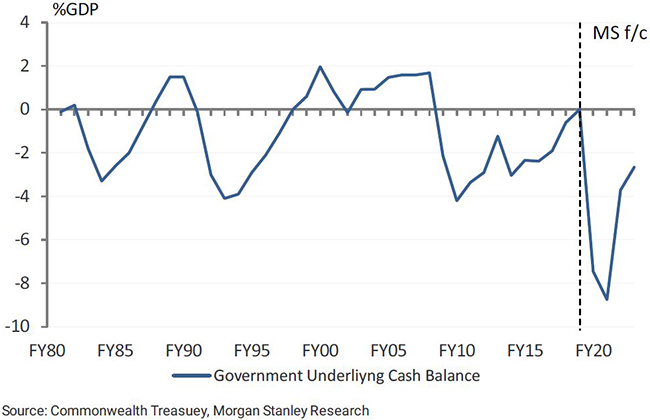

Exhibit 2: The federal government budget balance will move sharply into deficit from stimulus measures

Of more structural concern are the state government positions. Though they have not provided the same level of stimulus measures as the federal government, their revenue positions are much more structurally vulnerable.

In particular, the reliance on GST revenues in the near term will have a large impact, as will the stamp duty revenues that will be doubly hit from the decline in housing turnover and prices. As an example, 9% of the New South Wales government’s revenues in FY19 came from stamp duty, with 22% from the GST.

Both of these mean state budget balances are likely to face more sustained deterioration – or alternatively that stimulus measures from state governments may be more restricted.

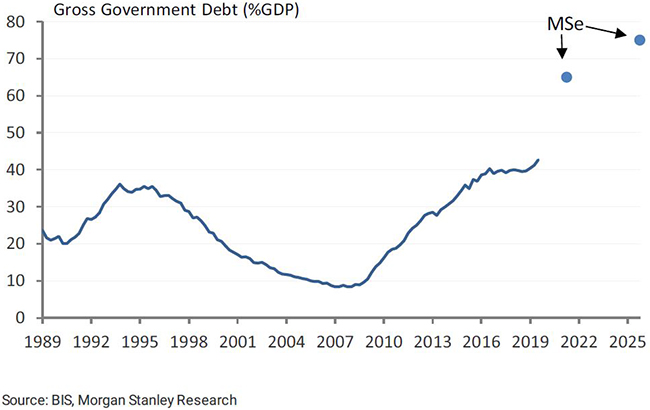

Combining this view of federal and state budgets suggests that government debt is likely to rise substantially from its current gross level of 43% of GDP to 65% of GDP.

Exhibit 3: We expect government debt to increase sharply to 65% of GDP over the next few quarters

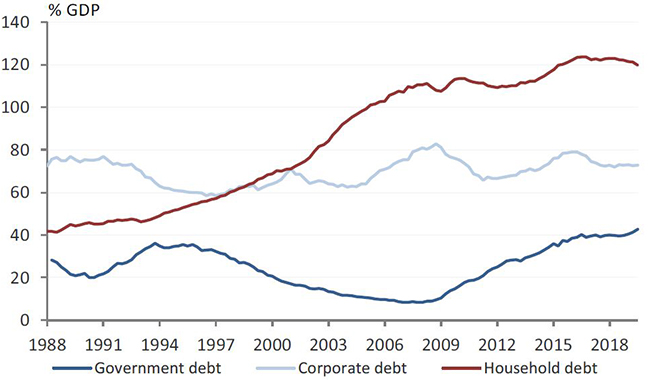

While government debt is expected to rise, Morgan Stanley Research expects Australian households to do the opposite, and that corporate debt is less of a concern in this crisis.

The level of Australian household leverage is one of the highest in the world at approximately 190% of income. This has supported growth in the past but it does make the economy vulnerable to an exogenous shock.

The economic slowdown in 2018/19 demonstrated that the Australian consumer is very sensitive to the housing market, and if there is a large downturn, then households are likely to face a simultaneous negative income and wealth shock.

This may lead households to concentrate on reducing debts over several years. This would improve their resiliency but slow the rate of recovery for the economy.

Morgan Stanley Research believes corporate debt is less of a concern in this crisis. Businesses came into this better capitalised than in the Global Financial Crisis. While around A$10 billion of listed capital has already been raised, and companies are likely to be more cautious, Morgan Stanley believes these changes are likely to be smaller than the adjustments in the household and government sectors.

Exhibit 4: Household debt remains larger, and persistent deleveraging is likely to slow the recovery

Inflation – Risks more to the downside

Another very active debate around recovery is the trajectory of inflation in Australia.

Morgan Stanley Research expects near-term dynamics to be disinflationary, due to the size of the initial demand shock, and forecasts deflation for the second quarter of 2020, largely driven by oil prices and policy changes.

A clear area of drag will be broader housing costs. These are one of the most persistent components of Australia’s consumer price index and make up 23% of the basket. A weaker housing market and higher vacancy rates will put downward pressure on rents, which could last for several quarters.

Over the more medium term, Morgan Stanley Research expects the risks to inflation are to the downside, due to a relatively slow recovery, persistently elevated unemployment rate, and mostly temporary government support. However, this may change if there is a more persistent increase in government spending and less household deleveraging than expected.

These views would also depend on the balance between the supply and demand contraction, and how much further support policymakers provide.

Summary: three structural issues in focus

Australia’s improved case trajectory enhances visibility of an activity trough and the focus is moving to recovery. Issues around migration, debt, and inflation are likely to persist after the direct virus impacts have eased.

Migration – up until now Australia has relied heavily on migration to drive growth, however there are risks in coming years due a slowing inflow of migrants.

Debt – while the Australian Government is expecting to increase its level of debt significantly, mainly due to a large stimulus package, it looks sustainable. The focus will move to debt reduction and reform. The fall in the housing market could drive sustained household deleveraging and a softer spending path. Corporate debt is less of a concern in this crisis.

Inflation – inflation is expected to weaken in both the short and medium term and persistent demand softness is likely to continue.

For more on the impacts of coronavirus, speak to your Morgan Stanley financial adviser or representative. Plus, more Ideas from Morgan Stanley's thought leaders.