Inflation expectations collapsed as the Great COVID-19 Recession (GCR) began and the demand for goods and services tumbled, but the recession should give way to a new cycle, one in which inflation will likely return.

Inflation returns

Better-than-expected growth data since May this year point to a faster-than-forecast recovery. Global manufacturing and services moved back into expansionary territory in July, retail sales in both the US and Europe are already close to, or above, their January 2020 peaks, and China will see an output of 3.3% above pre-COVID-19 levels this quarter.

Morgan Stanley economists project inflation to return in the next 12-24 months, sparked by four major pillars: One, a V-shaped recovery after a sharper but shorter recession. Two, a timely, sizeable and coordinated monetary and fiscal policy response to the COVID-19 shock. Three, increased scrutiny and disruption of the interplay between technology, trade and titans, a structural disinflationary force over recent decades. Four, a renewed and reinforced commitment of central banks to reach their inflation goals.

The US is likely to be the most exposed to the risk of higher inflation in this cycle, with personal consumption expenditures rising to 2.0% year-on-year by the end of 2021 from 1.6% year-on-year in December 2020. However, a swift return to pre-COVID-19 output levels across developed markets by the third quarter of 2021 is also likely to have implications for inflation dynamics in other industrial economies.

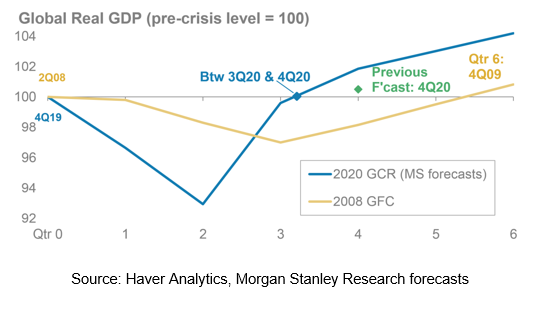

Morgan Stanley economists also expect global GDP to return to pre-COVID-19 levels in the fourth quarter of 2020 and in the second quarter of 2021 in the US, a substantially faster recovery than in the global financial crisis. The faster recovery should hasten economies' exit from disinflation as global output gaps close.

Sharper but shorter: Global GDP to reach pre-COVID-19 levels in 4Q20

Driving returns from inflation

What does higher inflation potentially mean for returns? Which assets could outperform when inflation rises? Which sectors may underperform in a reflationary environment?

Morgan Stanley’s analysis of the next 12-month cross-asset performance across four distinct inflation regimes – (1) Above average and rising, (2) Above average and falling, (3) Below average and falling, and (4) Below average and rising – finds that:

- Equities – do best when inflation is below trend and rising and nominal growth expectations rise; stocks do worst when inflation is above trend and falling, typical of a late-cycle environment.

- Equity sectors – global defensives underperform while cyclicals outperform in below-trend and rising inflation environments: Staples, utilities and health care are sectors which underperform the most when inflation is below trend and rising. On the contrary, this environment is best for cyclical stocks such as industrials and technology.

- Bonds – underperform when inflation is rising.

- Credit – outperforms when inflation is below trend and rising, a typical early-cycle dynamic. On the other hand, credit underperforms the most in a late-cycle environment when inflation is above trend and falling.

- USD – weakens as inflation falls. The bulk of the USD weakening usually happens when inflation is falling, with USD weakening the most against emerging markets currencies and JPY.

- Commodities – oil outperforms when inflation is below trend and rising while gold performs well when inflation is below trend and falling: Commodities are one of the most commonly known inflation hedges in the market, but this outperformance tends to happen as inflation rises from a low level.

Based on our economists' expectation of higher inflation over the next 12-24 months, the current 'below trend and falling' inflation regime is likely to shift to one of 'below trend and rising'. This has historically meant better equity and credit returns, outperformance of cyclical stocks over defensives, higher bond yields, weaker JPY, emerging markets’ foreign exchange outperformance and higher oil prices.

Reflation means reallocation to stocks – strategic asset allocation across inflation regimes

History suggests that strategic asset allocation will favour stocks over bonds, high-beta (more volatile) equity and fixed income sectors over defensives when inflation starts to rise.

But even before we think about valuations, how should an investor position for a reflationary environment? What is the 'right' strategic asset allocation for when inflation starts to rise? Does it just mean piling into assets whose returns are correlated with inflation? Not quite.

Inflationary regimes matter for portfolios not just in terms of how they impact expected returns, but also in how volatility and correlation environments tend to vary with inflation. The general rule of thumb is that when inflation is above average, portfolios should favour fixed income and low beta, while allocation to stocks and high beta rise in environments where inflation is below average.

What does this mean for investors?

With structural disinflationary forces being disrupted and inflationary pressures emerging by 2022, investors should be prepared for a potential pickup in inflation. Real assets, such as commodities and real estate, may serve as a more compelling alternative given their historical performance during inflationary periods.

Markets signals and key economic data to look out for include: a weakening USD dollar, a rise in CPI and/or inflation expectations, rise in the price of goods and raw materials such as oil, industrial metals and other commodities, rise in employment and wage growth, and additional fiscal and monetary actions from policy makers.

For more Morgan Stanley Research on the return of inflation, speak to your Morgan Stanley financial adviser or representative for the full report, “Hedges and Strategic Asset Allocation for Inflation Regimes" (2 Oct, 2020). Plus, more Ideas from Morgan Stanley's thought leaders.